All Categories

Featured

Table of Contents

- – How do I get started with an Annuity Payout Op...

- – Who should consider buying an Annuity Income?

- – What does a basic Long-term Care Annuities pl...

- – What should I know before buying an Fixed-ter...

- – Why is an Annuity Payout Options important f...

- – Is there a budget-friendly Lifetime Income A...

For those ready to take a little bit much more danger, variable annuities use additional possibilities to expand your retirement assets and possibly enhance your retirement income. Variable annuities give a variety of financial investment alternatives managed by expert money supervisors. As a result, financiers have more adaptability, and can also relocate properties from one alternative to one more without paying tax obligations on any kind of financial investment gains.

* An immediate annuity will not have a build-up phase. Variable annuities issued by Safety Life insurance policy Business (PLICO) Nashville, TN, in all states except New york city and in New York City by Safety Life & Annuity Insurer (PLAIC), Birmingham, AL. Securities provided by Investment Distributors, Inc. (IDI). IDI is the principal underwriter for registered insurance policy products released by PLICO and PLAICO, its associates.

Investors ought to meticulously consider the investment objectives, risks, charges and expenditures of a variable annuity and the underlying investment alternatives before spending. This and other info is included in the syllabus for a variable annuity and its hidden financial investment alternatives. Programs may be gotten by speaking to PLICO at 800.265.1545. An indexed annuity is not a financial investment in an index, is not a protection or stock market investment and does not take part in any supply or equity financial investments.

What's the difference between life insurance policy and annuities? It's an usual inquiry. If you wonder what it takes to protect an economic future on your own and those you enjoy, it may be one you locate on your own asking. And that's a great thing. The lower line: life insurance policy can assist supply your loved ones with the monetary comfort they should have if you were to die.

How do I get started with an Annuity Payout Options?

Both should be taken into consideration as component of a long-lasting monetary plan. Both share some resemblances, the overall objective of each is really various. Allow's take a glance. When contrasting life insurance policy and annuities, the most significant distinction is that life insurance policy is developed to aid secure versus a financial loss for others after your fatality.

If you intend to discover a lot more life insurance policy, reviewed up on the specifics of how life insurance policy works. Think about an annuity as a tool that could help meet your retired life demands. The main purpose of annuities is to create earnings for you, and this can be carried out in a few various ways.

Who should consider buying an Annuity Income?

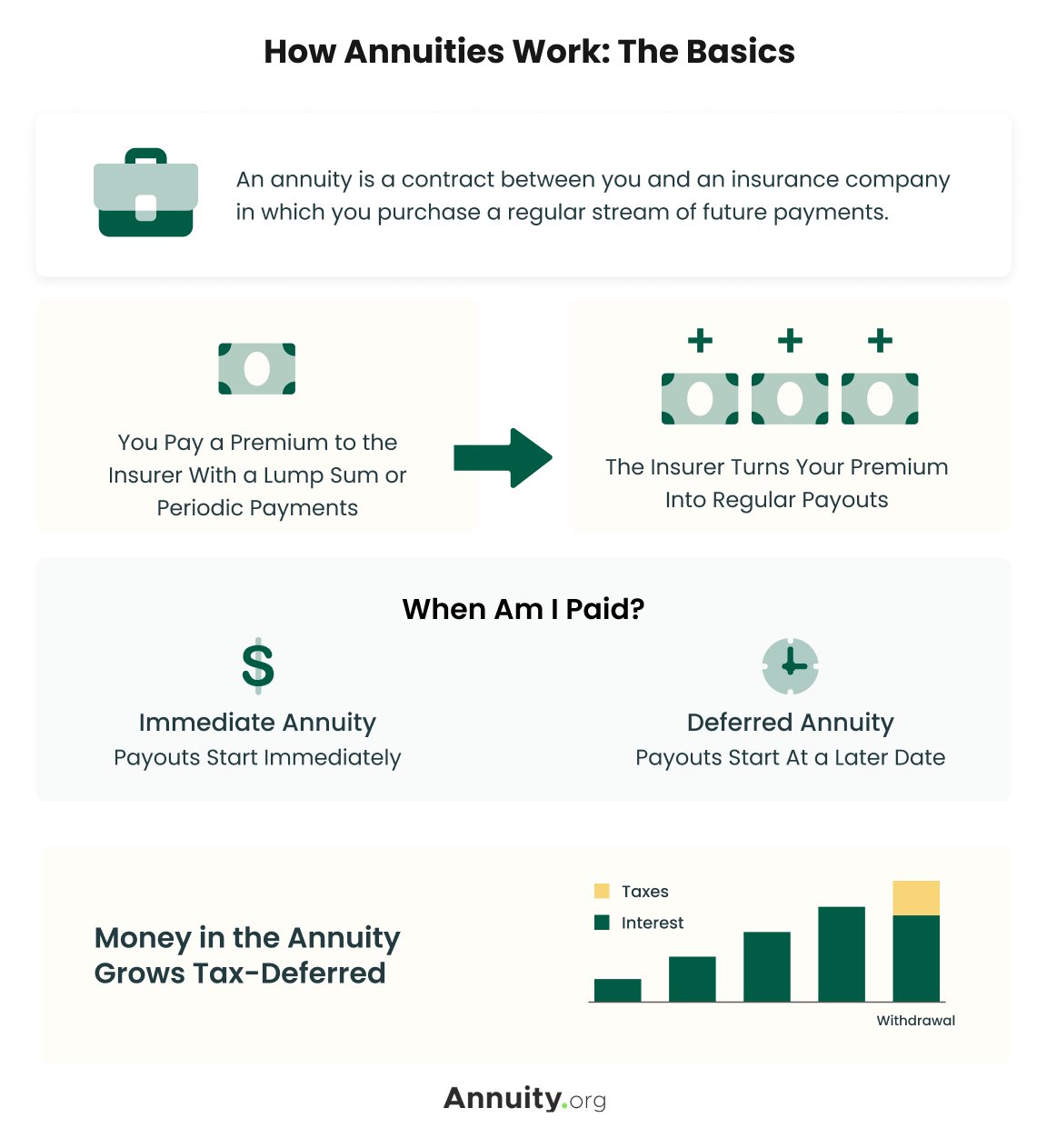

There are many potential benefits of annuities. Some include: The capacity to grow account value on a tax-deferred basis The capacity for a future income stream that can't be outlived The opportunity of a swelling sum benefit that can be paid to a making it through spouse You can buy an annuity by providing your insurance business either a single lump sum or paying with time.

Individuals generally purchase annuities to have a retirement revenue or to build savings for another function. You can acquire an annuity from a certified life insurance policy representative, insurance provider, financial coordinator, or broker. You should talk with a monetary consultant regarding your needs and objectives before you acquire an annuity.

What does a basic Long-term Care Annuities plan include?

The difference between both is when annuity payments begin. permit you to conserve money for retirement or various other factors. You don't need to pay taxes on your revenues, or contributions if your annuity is a specific retired life account (INDIVIDUAL RETIREMENT ACCOUNT), until you withdraw the revenues. permit you to produce an earnings stream.

Deferred and immediate annuities offer several alternatives you can pick from. The choices supply various degrees of possible risk and return: are assured to earn a minimum passion price.

permit you to select in between sub accounts that are comparable to shared funds. You can make more, yet there isn't a guaranteed return. Variable annuities are greater risk because there's a possibility you might shed some or all of your money. Set annuities aren't as risky as variable annuities due to the fact that the financial investment risk is with the insurance company, not you.

Fixed annuities ensure a minimal rate of interest rate, normally between 1% and 3%. The firm might pay a higher rate of interest price than the assured interest price.

What should I know before buying an Fixed-term Annuities?

Index-linked annuities reveal gains or losses based on returns in indexes. Index-linked annuities are extra intricate than fixed deferred annuities. It is very important that you understand the attributes of the annuity you're taking into consideration and what they indicate. The two contractual features that influence the amount of interest attributed to an index-linked annuity the most are the indexing method and the participation rate.

Each relies upon the index term, which is when the firm calculates the interest and credit reports it to your annuity. The determines just how much of the boost in the index will be used to calculate the index-linked rate of interest. Various other vital features of indexed annuities consist of: Some annuities cap the index-linked passion price.

Not all annuities have a flooring. All taken care of annuities have a minimum surefire value.

Why is an Annuity Payout Options important for long-term income?

The index-linked rate of interest is added to your initial premium amount but doesn't substance throughout the term. Various other annuities pay compound interest throughout a term. Substance passion is rate of interest earned on the money you saved and the interest you make. This indicates that passion already attributed likewise makes rate of interest. In either instance, the passion made in one term is normally intensified in the following.

This percent could be made use of rather of or along with an involvement price. If you secure all your money prior to the end of the term, some annuities will not attribute the index-linked passion. Some annuities may attribute just part of the passion. The percentage vested normally boosts as the term nears the end and is always 100% at the end of the term.

Is there a budget-friendly Lifetime Income Annuities option?

This is due to the fact that you birth the financial investment threat rather than the insurance provider. Your agent or financial adviser can help you choose whether a variable annuity is appropriate for you. The Securities and Exchange Compensation identifies variable annuities as safety and securities because the efficiency is stemmed from supplies, bonds, and other financial investments.

Discover more: Retirement ahead? Think of your insurance coverage. An annuity contract has two stages: a buildup stage and a payout stage. Your annuity gains passion during the accumulation phase. You have several options on exactly how you add to an annuity, relying on the annuity you acquire: allow you to select the moment and quantity of the repayment.

{kind=link}

Table of Contents

- – How do I get started with an Annuity Payout Op...

- – Who should consider buying an Annuity Income?

- – What does a basic Long-term Care Annuities pl...

- – What should I know before buying an Fixed-ter...

- – Why is an Annuity Payout Options important f...

- – Is there a budget-friendly Lifetime Income A...

Latest Posts

Decoding Retirement Income Fixed Vs Variable Annuity A Comprehensive Guide to Retirement Income Fixed Vs Variable Annuity Defining Pros And Cons Of Fixed Annuity And Variable Annuity Advantages and Di

Decoding Fixed Annuity Or Variable Annuity Key Insights on Tax Benefits Of Fixed Vs Variable Annuities Breaking Down the Basics of Fixed Vs Variable Annuities Advantages and Disadvantages of Retiremen

Understanding Financial Strategies A Comprehensive Guide to Investment Choices What Is the Best Retirement Option? Features of Smart Investment Choices Why What Is A Variable Annuity Vs A Fixed Annuit

More

Latest Posts